Fund Equity Info and Management

Understanding Fund Equity

Overview

Fund equity (FE) represents the net financial position of a specific cost center, reflecting the accumulated balance over time by combining the beginning fund equity balance, revenues, expenditures, and fund equity transfers.

In simple terms, fund equity shows whether a cost center has remaining funds available or has expended more than it has accumulated. It is commonly used to evaluate the financial health and sustainability of a cost center, fund, unit or university.

Fund Types

Not all funds operate under the same financial rules. Funds are classified into two main categories: Centrally Allocated Funds and Self-Supporting Funds.

Centrally Allocated Funds

These funds are supported by resources managed centrally by the university. Cost centers funded by centrally allocated sources are not required to maintain a positive cash or fund equity balance throughout the fiscal year, as any shortfall is covered during UHD’s cash transfer process at fiscal year-end (period 998).

In other words, UHD does not add fund equity into each centrally funded cost center at the beginning of the fiscal year to mirror the loaded expense budgets, nor does the university add fund equity into each centrally funded cost center during the fiscal year. Instead, UHD waits for final expenditure adjustments to post in period 998, and then the Budget Office transfers fund equity from the central revenue holding cost centers to the department expense cost centers.

Additionally, the UHD Budget Office manages all funds for the university to ensure the various sources are expended to the appropriate levels, have acceptable reserve balances, and follow state and UHS spending rules. As such, for fund management purposes it is common for the Budget Office to shift department budgets between fund codes, commonly referred to as budget swaps.

Cost centers funded by centrally allocated funds can carry a fund equity balance (think of it as a savings account) that can be carried forward into the next fiscal year and budgeted when desired by the department (see Carry Forwards section).

Self-Supporting Funds

These funds must always maintain a positive fund equity balance during the fiscal year. Cost centers in this category are expected to generate enough revenues to cover expenses. A fund equity deficit in a self-supporting cost center requires immediate attention (see Addressing Negatives section).

For a complete reference on fund types, please visit the Fund Codes page.

Understanding Fund Equity

The Fund Equity Report (also known as the 016 Report) provides a high-level view of the financial position of cost centers, including beginning fund equity balances, revenues, expenditures, in-year fund equity adjustments, and the resulting current fund equity balances.

Departments are encouraged to review this report regularly to monitor financial activity and maintain awareness of available resources or deficit balances.

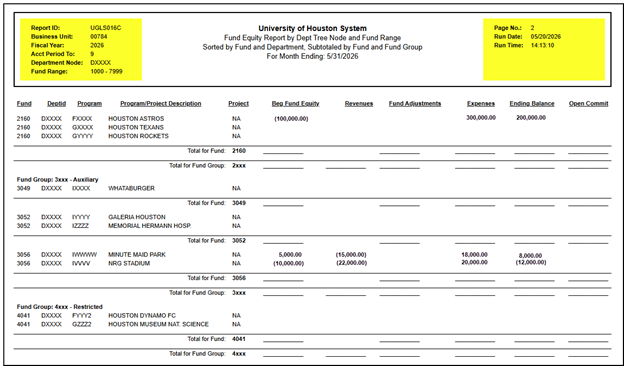

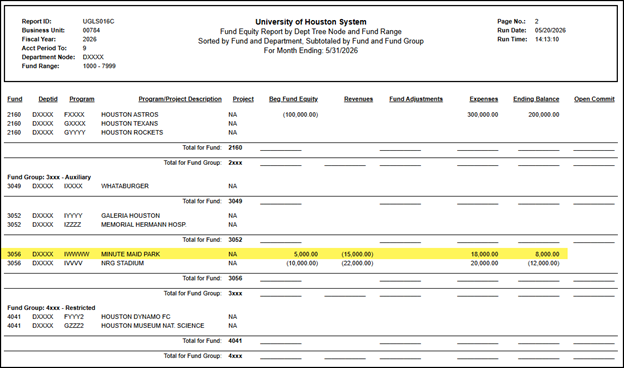

Once the Fund Equity Report has been generated, you will see a report similar to the example shown below (PDF format):

In the upper right-hand section of the report, users can identify the report parameters selected when generating the report.

In the upper left-hand corner, users can find the Report Time and Date, which indicates when the report was generated.

Key Components:

-

- Beginning Fund Equity Balance – Represents the fund equity balance posted at the end of the previous fiscal year. This amount reflects the cumulative result of all prior-year revenues, expenses, and adjustments. A negative value (an amount within parentheses) in this column indicates a positive balance.

-

- Revenues – Captures all revenues collected during the current fiscal year, such as fees, sales, gifts, endowment income and awards. A negative value (an amount within parentheses) here represents a positive net revenue received.

- Fund Adjustments - Reflects in-year fund equity adjustments such as transfers, corrections, or reclassifications

that affect the fund equity balance but are not classified as revenues or expenses.

A negative value (an amount within parentheses) represents a net increase to the cost center’s FE balance.

A positive value represents a net decrease to the cost center’s FE balance.

- Expenses – Reflects cumulative expenditures posted to the cost center during the fiscal year. A positive value indicates actual expenses incurred (reduces the cost center’s FE balance).

- Ending Balance - The result of combining the Beginning Fund Equity, Revenues, Fund Adjustments,

and Expenses. It represents the current net position of the cost center.

A value displayed in parentheses (negative) indicates a favorable balance, meaning the fund has available resources or a surplus.

A positive value, on the other hand, indicates a fund equity deficit that must be resolved before the end of the fiscal year.

- Open Commitments: Represents earmarked expense obligations but not yet expended. Since open commitments

are not recorded expenses, they are NOT included in the expenses amount under the

Expenses column, but should be expected to reduce the cost center’s fund equity once

the encumbrance turns into actual posted expenses.

Open commitment examples include purchase orders that have been issued but not fully paid, or expected employee salary & wages and fringe benefit costs through the rest of the fiscal year.

To better understand how to interpret these columns, below are three examples:

Example 1 – 2160-DXXXX-FXXX-NA - Houston Astros (Centrally Funded Cost Center): This cost center began the year with a Beginning Fund Equity of ($100,000.00), representing a positive FE balance of $100,000. After incurring $300,000 in expenses, the Ending Balance shows a negative balance of $200,000.00. Since this is a centrally funded cost center, the true available FE balance is calculated by starting with the original Beginning Fund Equity minus any budgeted carry forwards (budgeted fund balance) posted during the year, which can be found in the Budget Node Summary (revenue side) under node B4035 (see Carry Forwards section).

Example 2 – 3056-DXXXX-IWWW-NA - Minute Maid Park (Cash Deficit. Self- Supporting Cost Center): This cost center began the year with a $5,000.00 Beginning Fund Equity balance, a positive value indicating an existing $5,000 deficit carried forward. After collecting $15,000 in revenues and posting $18,000 in expenses, the current FE Ending Balance is $8,000.00, a cash deficit that must be resolved before fiscal year-end (see Addressing Negatives section).

Example 3 – 3056-DXXXX-IVVVV-NA - NRG Stadium (Surplus Position. Self- Supporting Cost Center): This cost center began the year with a Beginning Fund Equity of ($10,000.00), a positive FE balance of $10,000. After collecting revenues and managing expenses effectively, the current FE Ending Balance shows ($12,000.00) a favorable surplus of $12,000.

Carry Forwards and Fund Balance

Any cost center that has a positive Beginning Fund Equity balance whether centrally funded or self-supporting is eligible to be budgeted (via budget journal) and expended in the current fiscal year when necessary. The Budget Office refers to the process of budgeting all or a portion of a cost center’s beginning fund equity balance as a Carry Forward.

The 13th period of the fiscal year, also known as 998, starts in September and ends in October, allows for final fiscal year-end adjustments. Departments complete revenue/expense adjustments by September, and the Budget Office starts year-end cash transfers by October 1st and completes them by mid-October. UHD General Accounting in coordination with UH, completes year-end financial close by the end of October.

Budgeting fund balance, or processing a carry forward, is typically allowed on November 1st, at the earliest and can be processed as needed throughout the fiscal year.

The Budget Office will notify departments when budget journals can be submitted to budget fund balance.

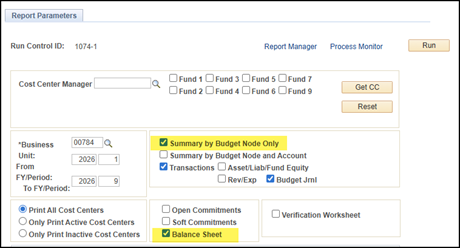

To calculate how much fund balance is available to carry forward, departments must run a 1074 report and include the following two pages:

-

- Summary by Budget Node Only

- Balance Sheet

Once the 1074 has been pulled, the available carry forward amount is determined using the following formula:

Formula for Available Fund Equity to Carry Forward:

Fund equity figure under the Beginning Year Balance column

less

the B4035 budget on the Budget Node Summary page

On the Balance Sheet, the amount that displays the cost center’s beginning year fund equity balance is listed on the Fund Equity row near the bottom of the Beginning Year Balance column, NOT the FE figure adjusted for open commitments at the very bottom.

The balance on the fund equity row is the intended result of a calculation during fiscal year-end cash transfers processed by the UHD Budget Office.

This amount, when displayed as a negative value, represents a positive available balance. Once 998 year-end processes are finalized, the beginning fund equity figure will never change during the current fiscal year.

Budgeting/adjusting a cost center’s fund balance budget (budget node B4035) does not adjust the cost center’s fund equity.

Similarly, adjusting a cost center’s fund equity does not adjust a cost center’s budget.

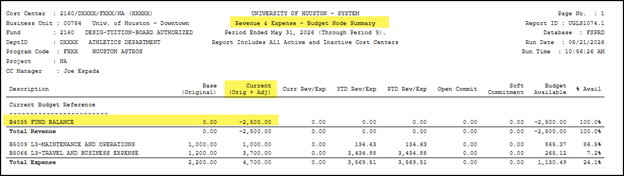

If carry forwards have been processed in a cost center, the B4035 (Fund Balance) budget node will be found on the Budget Node Summary page of the 1074 report, under the Current budget column.

The B4035 budget represents the cumulative effect of carry forwards budgeted during the current fiscal year. The B4035 budget should never exceed the cost center’s beginning fund equity balance. In other words, the most fund balance that can be budgeted in a cost center is its beginning fund equity balance.

To calculate how much fund equity has not been budgeted in the current fiscal year, the B4035 budget must be subtracted from the cost center’s beginning fund equity balance. Failing to subtract the current fund balance budget from the beginning FE balance may lead to overspending, or double spending.

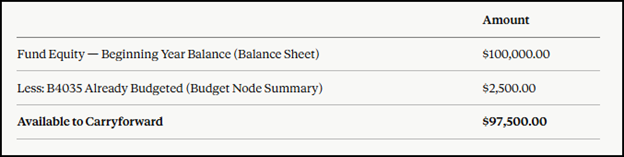

Using the Houston Astros cost center as an example:

In this case, the department has already processed $2,500.00 in carry forward budget journals and still has $97,500.00 available to carry forward for the remainder of the fiscal year.

Important: The available carry forward balance decreases each time B4035 is budgeted. Departments should re-run the 1074 report periodically to ensure they have an up-to-date picture of their remaining balance before submitting additional carry forward journals.

Addressing Fund Equity Negatives

Self-supporting cost centers must be actively monitored throughout the fiscal year to ensure they maintain a positive balance, both in budget and in cash (fund equity). There are two ways to check the current cash position of a cost center:

-

- Run the Fund Equity Report (as shown earlier) and review the Ending Balance

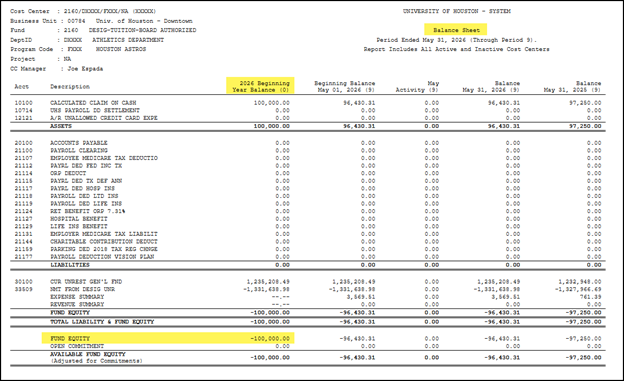

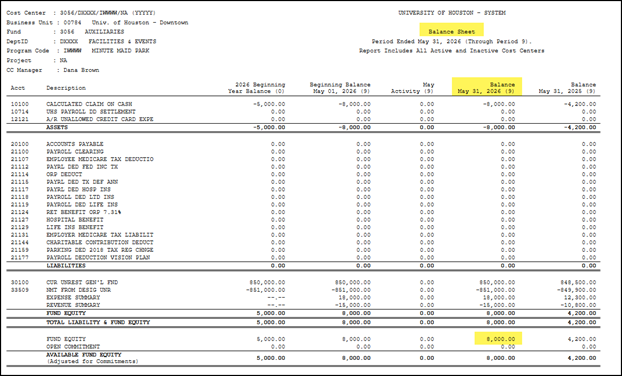

- Run the 1074 report and navigate to the Balance Sheet The fourth column will reflect the cost center's current cash position at the time the report is run. Specifically, review the Fund Equity line at the bottom of the report.

To illustrate, the example below walks through the Minute Maid Park cost center. As shown below, the Fund Equity Report reflects a cash deficit of $8,000 under the Ending Balance column. The same figure can be confirmed on the Balance Sheet page of the 1074 report, where the Fund Equity line (highlighted below) shows the same $8,000 positive value, which in this report's format indicates a deficit that must be resolved before the end of the fiscal year.

Fund Equity Report

1074 Report – Balance Sheet

Resolving a Negative Cash Balance

When a self-supporting cost center has a fund equity deficit, determine if additional revenue will be collected.

If additional revenue will not be collected, expenses should be relocated to another cost center(s).

-

-

- Payroll expenses — Through payroll reallocations submitted via an eRAF (electronic Reallocation Form).

-

For the step-by-step guide, please follow the following link: Payroll Reallocations

-

-

- Non-Payroll expenses — Through a GL journal entry for non-scholarship awards or through the scholarship portal/Campus Solutions for scholarship awards.

-

For guidance on how scholarship awards should be moved, please follow the following link: Scholarships